Creating scenarios

Scenarios FAQ

This is where the magic is.

Before you can generate a scenario, you've got to have at least some data in the system. Refer to the Quickstart Guide to get up and running quickly.

Scenarios are where you can play "what if". What if I paid only the minimum fees? What if I only sent an extra $20 to one of my credit cards? What if I followed Debtinator's advice and paid things down in Highest Interest Order? What if I paid things down by DOLP Score?

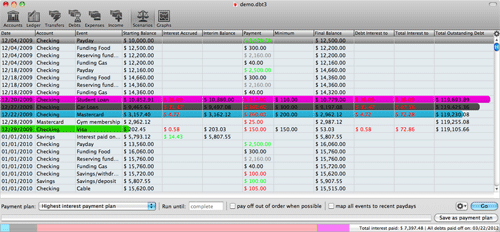

Run a scenario

- Go the Scenarios pane (second from the right in the toolbar). Choose the payment plan you want, and hit Go.

- You might need to go get a cup of coffee at this point. The calculations involved can be pretty intense, depending upon how your finances are structured. Some people can have their report finish in seconds, others may take hours. Realistically? Most reports take less than 5 minutes to complete. But if you have a lot of complicated information or a slow computer, it may take a while.

- Once it's complete, you can see the report of how to pay down your debts. It'll tell you the date an event occurs, what it was, which bank account it impacts,

any interest accrued, the payment you're expected to send, how much you're paying towards the principal of your debts, your outstanding debt, and on and on.

By default, only the 12 most frequently needed columns are visible, but if you hit the little gear button in the upper right of the table, you can customize what you see. So add in as much or as little information as you need.

- You can customize further by hitting the filtering gear in the lower right by the "Go" button. This will allow you to only see certain events. For example, you might just want to pay attention to a single credit card. You can filter down to just that one. Or you might want to only look at times when you're making overpayments. You can filter to that, too.

- There are a couple of options for running the reports, too:

- You can specify a "Run until" date. This will end the report at the given point in time. Be careful! If you stop a report before all debts are paid off, then Debtinator may not properly set aside funds for later bills. If you always run until it's complete, then it'll be sure that it can always pay everything.

- Pay off out of order when possible - Sometimes, you just don't want to stick quite to the plan. It's nice to knock out that credit card that's only got

a $100 balance on it, even though it has a lower interest rate on it. So you can check to pay off a debt when it can, even if it varies from the specified report.

This will usually cost you a little bit of extra money, but gives you satisfaction of paying something off quicker.

- map all events to recent paydays - you can specify on the Debts and Expenses panes to map bills to recent

paydays. Say your credit card is due on the 15th of the month, but you get paid on the 10th. You might as well just pay the bill on the 10th, otherwise you've just got

money sitting around in your account doing nothing. Plus, that way you won't accidentally spend it later.

You can bind specific events to paydays by editing them directly, or override it for all events and bind them all here. Use whichever works for you, or a combination of both.

- When a scenario is done running, it'll show you in the lower right how much interest was paid, as well as the date you're out of debt. To compare a lot of scenarios

at once, it's usually easier to go to the Graphs Pane. By plotting out multiple scenarios at once, it will also tell you which one will save

you the most money.

On the bottom left is a stacked barchart that shows you how much debt you have at that point in time. If you select a row in the report, the barchart will adjust to show how much debt was left by then. Mouseover the barchart to see how much is left on each debt.

- Once you've figured out the scenario you like the most, you can save it as a payment plan. That will move it over to the Ledger Pane so you can just click on things to apply them to your transaction ledger. See Working with Transactions for more info.

Available scenarios

You have a number of scenarios to consider. The minimum fee plan is always your worst case scenario - all of the other plans will always get you out of debt more quickly. But from there, it's up to you. If you want to save the most money? Try the Highest Interest Payment Plan. Want to reduce the number of debts you have the fastest? Try the Lowest Balance Payment Plan? Want to finely control exactly how much you send to a debt? The User Defined Overpayment plan it is. Use a scenario that not only saves you money, but fits in with how you would like to accomplish your financial goals.

Underlined scenarios tend to perform very well

- Lowest interest payment plan - excess funds pay off the debt with the lowest interest rate first. This is usually pretty bad.

- Highest interest payment plan - excess funds pay off the debt with the highest interest rate first. This is almost always the best approach.

- Lowest possible interest payment plan - excess funds pay off the debt with the lowest possible interest rate first. This is usually pretty bad.

- Highest possible interest payment plan - excess funds pay off the debt with the highest possible interest rate first. This is frequently the best approach. Note that if interest rates don't vary over time, this will match the highest interest payment plan.

- Lowest balance payment plan - excess funds pay off the debt with the lowest balance first. This is a good way to knock out smaller debts quickly so you don't need to worry about them, but overall savings are mixed.

- Highest balance payment plan - excess funds pay off the debt with the highest balance first. Quality varies, it's usually only for comparison purposes.

- Lowest fees payment plan - excess funds pay off the debt with the lowest monthly fees first. This is usually pretty bad.

- Highest fees payment plan - excess funds pay off the debt with the highest monthly fees first. This is usually a very good approach, but tends to lose out to the highest interest approach.

- Lowest possible fees payment plan - excess funds pay off the debt with the lowest possible monthly fees first. This is usually pretty bad.

- Highest possible fees payment plan - excess funds pay off the debt with the highest possible monthly fees first. This is usually a very good approach, but tends to lose out to the highest interest approach.

- Lowest minimum payments payment plan - excess funds pay off the debt with the lowest required payments first. This varies in quality.

- Highest minimum payments payment plan - excess funds pay off the debt with the highest required payments first. This varies in quality.

- Lowest possible minimum payments payment plan - excess funds pay off the debt with the lowest possible required payments first. This varies in quality.

- Highest possible minimum payments payment plan - excess funds pay off the debt with the highest possible required payments first. This varies in quality.

- Even split payment plan - Excess funds are divvied up and extra money is sent evenly to all debts. This report can have good results, but it varies wildly.

- All cash on hand payment plan - However much money you can spare goes to whatever debt comes due first. This report can have good results, but is highly variable depending upon the data.

This report is a good one to use if you're afraid that you'll waste the money in your bank account. As soon as it can get rid of money, it will. You can get similar effects and possibly better performance by using the highest interest plan and binding to recent paydays, though.

- User defined payment plan - Debts are paid off in the order they are listed in the debts screen. Drag and drop debts on that screen to re-order them. This can be a very good report - for example, your mortgage payment may be your highest interest rate, but it still make more sense to pay off a lower rate credit card first, to reach the point where your debt is only the house. Ordering the debts from highest to lowest interest rate, with the mortgage on the bottom may be cost effective.

- User defined overpayment plan - This allows the user to pay off debts by the maximum payment defined. A lot of people insist upon handling their payment strategies themselves. They want to send an extra $20 to a credit card, and $50 to the car, and $100 to the mortgage. This allows it. Set the maximum payments for those debts to how much you want to pay, and they'll all be overpaid, as possible. If no maximum payment is defined, it'll send the minimum.

- Lowest Minimum Fee/balance ratio plan - Debts are paid off based upon which debt has the highest balance/minimum fee ratio. The rationale is that the debts with the highest ratio tend to be farthest from being paid off, so they should be targeted first. This approach varies in quality.

- Lowest DOLP score payment plan - Debts are paid off in the same order they would be paid off if you only sent the minimum payments. That is, they are ordered by the number of minimum payments required to pay off the debt. This can have decent results if all of your cards have comparable interest rates. Regardless, it will usually be the quickest at freeing up money.

- Lowest DOLP score payment plan - Debts are paid off in the reverse order they would be paid off if you only sent the minimum payments.

- Minimum fee only payment plan - Excess funds are banked instead of paying your debts, and only the minimums are paid. This is an utter disaster. Any of the other approaches will save you hundreds or thousands

of dollars over this approach. Don't be fooled by the fact that this scenario will show you having more money in the bank than any of the other ones will.

That's because the minimum fee plan inevitably takes years longer to complete. If you graph bank account balance over time, you can see it in action. The minimum fee plan will keep more money in the bank in the short term, but long term you'll lose out.

- Why does this scenario take so long? Why do the graphs take so unbelievably long?

- You've entered a lot of data. Debtinator will have to analyze it, extrapolate it, crunch it, and whatever other metaphor you like. But there's a lot of processing involved in it, so it can take a while. Just sit back and relax, maybe go get a cup of coffee while it runs. We do recommend either printing out or exporting your report data once it's been run, so you don't need to sit through it again. Graphs need to crunch even more data, so they take much longer. For instance, a graph that contains all 7 report types needs to run all 7 reports. Much more processing time, much longer run time. You can always use Debtinator to budget in money to upgrade your computer! :-)

- How can I get my data out of a scenario?

-

You have several options. You can go to the File menu and choose Export. There, you can export as a tab delimited data file (ASCII or UTF-8), which can be imported into Excel or the like. Or, you can

export an iCal calendar file. You can then double click on it, and iCal will populate with the payment plan you generated. This way you can get calendar alerts as things come do.

Or you can simply select the rows you're interested in, copy them, and paste them wherever you want.

- Debtinator said that next month my credit card would have a balance of $994.68. The bank says it's $997.22. Is there a bug in your program?

-

No. The bank is simply compounding the interest differently than Debtinator is. Right now, we compound using the last balance (which

is usually the average daily balance), over the timeframe specified. Your bank may use a different balance (highest, lowest, average, median, etc.),

or compounding schedule (bills monthly, compounds biweekly; compounds continuously, etc.). Just update Debtinator from time to time with official statements and you should be

okay. Future versions will support more compounding options.

Rounding errors may also add up (for example, if Debtinator rounds and then adds and your bank adds and then rounds, there can be slight variance). So slight variance is to be expected. As always, don't panic. If you see a discrepency, note it in the app. If it's a big one or you're really concerned, shoot us an email

- Isn't this program 100% accurate?

-

No, but it's close enough. We're talking about large quantities of money calculated various ways over multiple years.

There will be some difference between the way Debtinator calculates vs the way the bank calculates. Also, Debtinator

assumes you'll be doing things like paying "$26.18" to a given credit card. Realistically? You'll probably pay a whole

value like "$26.00" or even "$25.00". So that will also cause slight variation.

It's still going to be close enough. When it comes down to it, if after 5 years it turns out you only saved $4,873 in interest instead of $5,019, it shouldn't be the end of the world. - My minimum payment varies from month to month. How do I handle that?

- Choose the complex debt screen and edit the minimum payment as appropriate. Show me how.

- Sometimes my reports (or graphs) are lightning fast, and sometimes they take a while. What gives?

- Debtinator will cache reports once they're run, since there's no need to redo the work all the time. But, the cache only remains valid so long as you make no changes to your data. Note that any changes will invalidate the cache - if you go back and change an account name, the cache is flagged invalid. It doesn't need to be only related to the numeric data.

- The even split report doesn't evenly split! The first debt got paid an extra $500, and the second only got paid $375! What gives?

-

I honestly haven't decided if I want to call this a bug or a feature, but the even split report calculates the percentage of money at

that moment in time. So let's say you have 4 debts, and $2000 in surplus cash. The first debt is due on the 5th of the month, and the

report will hit it and evenly divide the funds and send it an extra $500. The next debt is due on the 8th of the month, but

by that point you only have $1500 in surplus cash. So it once again divides up the money and sends it an extra $375. You now have

$1125 in the bank, so the next debt would get an extra $281.25, and so on.

Extra expenses or income in the middle just complicates things and decreases the excess further. So file this under "known, expected behavior", but it may change in the future.

- My report says I ran out of money! What gives?

- It means you ran out of money, but don't worry! You know about it now, so you can deal with it. Check the Scenario troubleshooting section for some suggestions on what to look for.

- How can I create an amortization table?

- Debtinator isn't quite the best tool to use for this, but nonetheless can create a table for you. To do it, go to the reports screen and run the "Minimum Payments Plan" report. Click the little gear button next to the go button and choose "Include none". Then, click it again and select the debt you wish to view. This will now be an amortization table of how long it'll take the single debt to be paid off. You can then customize any report columns you'd like to see.

- Hey! I had a credit card that was owed $700, and I had $10,000 in the bank and it didn't pay it off! What gives?

-

Your credit card doesn't meet the criteria to be paid off first. For example, you may be running the highest interest payment plan,

but your credit card is the second highest. So it gets skipped in favor of paying off the later debt.

It usually evens itself out after a month or so. In exceptional circumstances, you may want to try moving up the due date of later (and higher interest!) debts to ensure that they get attacked and paid down first, but that only applies for unique combinations of data. If you think a report is inaccurate or you're paying too much, please drop me a note and I'll try to help you work through how to make it more efficient.

I'd really love to include some fancy FAQ based solution for how to fidget the data to even out minor hiccups like this, but it varies so much it needs to be addressed individually.

- Debtinator rarely pays my account down to $0, so I've just got wasted money sitting in my account. Isn't it always supposed to? Why doesn't it pay towards my debt?

-

Debtinator will budget for the future. For example, say that you have to pay property tax on your

house once a year, and to make the math easy it's $1200. Roughly on a per monthly basis, Debtinator will keep an extra $100 in your account instead of

putting it towards your debt, because it needs to save that money up to pay for the tax bill at the end of the year. So that will keep your account

from going down to zero.

Of course, it's also possible that you found one of the myriad edge cases that could cause the program to get confused and not pay down to zero when it should. If that's the case, then please let me know! I always want to fix those. Basically, my assumption is that as long as the program shells out all of your money at least once, then it's running correctly, and other times when it's leaving money in the bank it's due to budgeting for the future. - Highest interest? Highest possible interest? What's the difference?

-

There are some variations on a few of the reports, such as "highest interest payment plan" vs. "highest possible interest payment plan", they sure sound similar and they are pretty close a lot of the time.

The variation is that the "regular" version looks at the current value, whereas the "possible" version looks at the highest one that could hit in the future, assuming the current balance hasn't decreased.

Examples help. Let's say you have two debts, a credit card at a 5% interest rate, and a second credit card with a 3% teaser rate that lasts for the next 6 months but then escalates to 20%. The highest interest payment plan will pay credit card #1 because it's currently at 5%, whereas the second card is at 3%. 6 months from now, it will re-allocate its funds to pay down the second card when the rate shoots up to 20%.

If you run the highest interest possible report, Debtinator will realize that the second card will go up to 20% in the future, so it will start paying it off immediately and keep the 5% card at the minimum.

On a related note, say that the first card is 5% forever, and the second is 5% but increases to 20% in 6 months. Starting with v2.2.1, Debtinator is smart enough to realize that even though both cards have the same rate right now, it should focus its money towards the second card to cut it down as much as possible before the higher rate hits.

If your interest rates are fixed, that is if you have two cards that are both at 5% forever, then there will be no difference between the "regular" and "possible" plans.

As always, your mileage may vary, so we recommend trying both out and seeing which one's more useful to you.

- What's the difference between Final Account Balance and Total Available Funds?

-

Final Account Balance is the money you have in the account from which you're paying the debt. So if you're paying your mortgage out of your checking account,

this is the amount of money left in checking when you're done.

Total Available Funds is the amount of money you have in all accounts (your checking account and savings account, for example) - What's the difference between Lowest Balance Payment Plan and Lowest DOLP score payment plan? They sound the same!

-

DOLP stands for "Dead On Last Payment". It's a way to order your payments based upon payoff order if you'd only sent the minimum payments. For example,

say you have two debts:

Name Balance Interest Rate Minimum payment Number of payments required (DOLP score) International Credit Card $1,000 0% $5 200 Store Credit Card $5,000 0% $500 10

I cheated and made the math easy by giving them both 0% interest rates. If you paid off in Lowest Balance order, excess money would be sent to the International Credit Card and pay it off first. If you pay off in Lowest DOLP score order, excess money would be sent to the Store Credit Card, since that's the one you'd be paying off first anyway. - Why do I have to include the minium payment plan when graphing bank account balance over time?

-

It makes my life easier. The minimum payments plan is guaranteed to be the farthest out in the future, so we use that as the date to normalize against.

Otherwise, we'd only run the plans until they finish (like the other graphs), and we'd end up stopping them short. It doesn't really work to compare

how much money you'd have on June 6th, 2010 with the highest interest plan vs how much money you'd have with the minimum payment plan in 2039.

Note that your bank account will always increase fastest with the minimum payment plan, but the other approaches will catch up and overtake it, hopefully quickly. - Transferring all available funds makes my report run really really slow. What gives?

- It's a known issue - we're working on it.

- I want to pay my expenses with a credit card, but make sure it's paid off every month. How can I do that?

- For the credit card you're using, set its minimum payment to 100% of the balance. That way it will always be paid when payment is due.

It's not uncommon to run a report and get an error like the following:

Out of Money

You ran out of money

Electricity is short by $80

Is this a bug in Debtinator? No! At some point, your expenses will exceed your income, and despite the program's best efforts, it couldn't figure out how to keep you afloat. Sure, it's upsetting and a concern that you're going to be short on paying your bills at some point, but at least you know about it now, so you can take steps to correct the situation.

So...now what do you do? Well, everyone's financial picture is different, but here are some general tidbits to help troubleshoot and track down what's going on.

- Look at the report. It'll run up until you run out of money and display everything up until then. Now's the time to look at your expenses and see if you can cut back. Yes, yes, we don't like to lecture about budgeting and living your life and all, but in this case, we make an exception. Without changes in your lifestyle, you'll run out of cash. Now's the time to go back and really evaluate things. Do you really need to spend $100/month going to the movies? Is food really going to cost you $200/week? Does your clothing budget really need to be $500/month? Cut back on those fungible expenses, even a little bit, and re-run the report. Maybe spending $80/month on movies is all you need to do.

- Check other accounts. Debtinator won't try to move funds around to cover things. So if your checking account runs out of money, but you have thousands in savings, Debtinator won't try to use it. If you have money in your savings account to cover it, then transfer it over. You can even set up a transfer to run the day before you run out of cash to move the funds into place automatically at the last moment.

- If you run out of cash immediately at the start, you probably haven't been paid yet. This is the most common issue. Let's say that you download and set up the program on April 26th, telling it that your next payday is April 27th, and you're paid weekly.. You run your reports, all is peachy. You come back the next day and try to run a report, and you'll immediately run out of money. That's because the app has advance your next payday to May 4th, assuming you've already been paid. You'll need to manually go fill in those funds to your bank account balance to get them to show up. Then you can re-run.